Question: The Lawndale Company pays $700 for insurance coverage received over the past few months. In this case, though, the amount has already been recognized by the company. Both the insurance expense and an insurance payable were recorded as incurred. Thus, the amounts can be seen on the trial balance in Figure 4.3 “Balances Taken From T-accounts in Ledger”. Apparently, Lawndale’s accounting system was designed to recognize this particular expense as it grew over time. When an expense has already been recorded, what journal entry is appropriate at the time actual payment is made?

Answer: Because of the previous recognition, the expense should not now be recorded a second time. Instead, this payment reduces the liability that was established by the accounting system. Cash—an asset—is decreased, which is shown by means of a credit. At the same time, the previously recorded payable is removed. Any reduction of a liability is communicated by a debit. To reiterate, no expense is included in this entry because that amount has already been recognized.

Note that Journal Entries 2 and 5 differ although the events are similar. As discussed previously, specific recording techniques can be influenced by the manner in which the accounting system has handled earlier events. In Journal Entry 2, neither the expense nor the payable had yet been recorded. Thus, the expense was recognized at the time of payment. For Journal Entry 5, both the expense and payable had already been entered into the records as the amount gradually grew over time. Hence, when paid, the liability is settled but no further expense is recognized. The proper amount is already present in the insurance expense T-account.

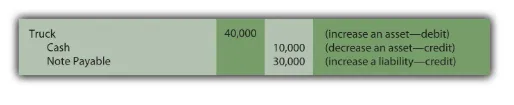

Question: Assume that a new truck is acquired by the Lawndale Company for $40,000. Cash of $10,000 is paid now but a note payable—due in several years—is signed for the remaining $30,000. This transaction impacts three accounts rather than just two. How is a journal entry constructed when more than two accounts have been affected?

Answer: As has been discussed, every transaction changes at least two accounts because of the cause and effect relationship underlying all financial events. However, beyond that limit, any number of accounts can be impacted. Complex transactions often touch numerous accounts. Here, the truck account (an asset) is increased and must be debited. Part of the acquisition was funded by paying cash (an asset) with the decrease recorded as a credit. The remainder of the cost was covered by signing a note payable (a liability). A liability increase is recorded by means of a credit. Note that the debits do equal the credits even when more than two accounts are affected by a transaction.

Question: Lawndale Company needs additional financing so officials go to current or potential shareholders and convince them to contribute cash of $19,000 in exchange for new shares of the company’s capital stock. These individuals invest this money in order to join the ownership or increase the number of shares they already hold. What journal entry does a business record when capital stock is issued?

Answer: The asset cash is increased in this transaction, a change that is always shown as a debit. Capital stock also goes up because new shares are issued to company owners. As indicated in the debit and credit rules, the capital stock account increases by means of a credit.

Question: In Journal Entry 4A, a sale was made on credit. An account receivable was established at that time for $5,000. Assume that the customer now pays this amount to the Lawndale Company. How does the collection of an amount from an earlier sales transaction affect the account balances?

Answer: When a customer makes payment on a previous sale, cash increases and accounts receivable decrease. Both are assets; one balance goes up (by a debit) while the other is reduced (by a credit).

Note that cash is collected here but no additional revenue is recorded. Based on the requirements of accrual accounting, revenue of $5,000 was recognized previously in Journal Entry 4A. Apparently, the revenue realization principle was met at that time, the earning process was substantially complete and a reasonable estimation could be made of the amount to be received. Recognizing the revenue again at the current date would incorrectly inflate reported net income. Instead, the previously created receivable balance is removed.

Comments are closed