The ‘Law Of Demand’ states that, all other factors being equal, as the price of a good or service increases, consumer demand for the good or service will decrease, and vice versa.

Demand elasticity is a measure of how much the quantity demanded will change if another factor changes.

Changes in Demand

Change in demand is a term used in economics to describe that there has been a change, or shift in, a market’s total demand. This is represented graphically in a price vs. quantity plane, and is a result of more/less entrants into the market, and the changing of consumer preferences. The shift can either be parallel or nonparallel.

Extension of Demand

Other things remaining constant, when more quantity is demanded at a lower price, it is called extension of demand.

| Px | Dx | |

| 15 | 100 | Original |

| 8 | 150 | Extension |

Contraction of Demand

Other things remaining constant, when less quantity is demanded at a higher price, it is called contraction of demand.

| Px | Dx | |

| 10 | 100 | Original |

| 12 | 50 | Contraction |

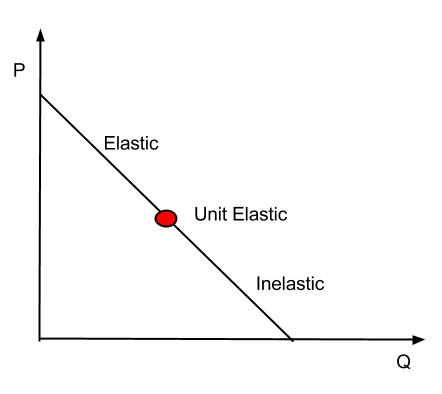

Concept of Elasticity

Law of demand explains the inverse relationship between price and demand of a commodity but it does not explain to the extent to which demand of a commodity changes due to change in price.

A measure of a variable’s sensitivity to a change in another variable is elasticity. In economics, elasticity refers the degree to which individuals change their demand in response to price or income changes.

It is calculated as −

Elasticity =

% Change in quantity% Change in price

Elasticity of Demand

Elasticity of Demand is the degree of responsiveness of change in demand of a commodity due to change in its prices.

Importance of Elasticity of Demand

● Importance to producer − A producer has to consider elasticity of demand before fixing the price of a commodity.

● Importance to government − If elasticity of demand of a product is low then government will impose heavy taxes on the production of that commodity and vice – versa.

● Importance in foreign market − If elasticity of demand of a produce is low in the international market then exporter can charge higher price and earn more profit.

Methods to Calculate Elasticity of Demand

Price Elasticity of demand

The price elasticity of demand is the percentage change in the quantity demanded of a good or a service, given a percentage change in its price.

Total Expenditure Method

In this, the elasticity of demand is measured with the help of total expenditure incurred by customer on purchase of a commodity.

Total Expenditure = Price per unit × Quantity Demanded

Proportionate Method or % Method

This method is an improvement over the total expenditure method in which simply the directions of elasticity could be known, i.e. more than 1, less than 1 and equal to 1. The two formulas used are −

iEd =

Proportionate change in edProportionate change in price

×

Original priceOriginal quantity

Ed =

% Change in quantity demanded% Change in price

Geometric Method

In this method, elasticity of demand can be calculated with the help of straight line curve joining both axis – x & y.

Ed =

Lower segment of demand curveUpper segment of demand curve

Factors Affecting Price Elasticity of Demand

The key factors which determine the price elasticity of demand are discussed below −

Substitutability

Number of substitutes available for a product or service to a consumer is an important factor in determining the price elasticity of demand. The larger the numbers of substitutes available, the greater is the price elasticity of demand at any given price.

Proportion of Income

Another important factor effecting price elasticity is the proportion of income of consumers. It is argued that larger the proportion of an individual’s income, the greater is the elasticity of demand for that good at a given price.

Time

Time is also a significant factor affecting the price elasticity of demand. Generally consumers take time to adjust to the changed circumstances. The longer it takes them to adjust to a change in the price of a commodity, the lesser price elastic would be to the demand for a good or service.

Income Elasticity

Income elasticity is a measure of the relationship between a change in the quantity demanded for a commodity and a change in real income. Formula for calculating income elasticity is as follows −

Ei =

% Change in quantity demanded% Change in income

Following are the Features of Income Elasticity −

● If the proportion of income spent on goods remains the same as income increases, then income elasticity for the goods is equal to one.

● If the proportion of income spent on goods increases as income increases, then income elasticity for the goods is greater than one.

● If the proportion of income spent on goods decreases as income increases, then income elasticity for the goods is less by one.

Cross Elasticity of Demand

An economic concept that measures the responsiveness in the quantity demanded of one commodity when a change in price takes place in another good. The measure is calculated by taking the percentage change in the quantity demanded of one good, divided by the percentage change in price of the substitute good −

Ec =

ΔqxΔpy

×

pyqy

● If two goods are perfect substitutes for each other, cross elasticity is infinite.

● If two goods are totally unrelated, cross elasticity between them is zero.

● If two goods are substitutes like tea and coffee, the cross elasticity is positive.

● When two goods are complementary like tea and sugar to each other, the cross elasticity between them is negative.

Total Revenue (TR) and Marginal Revenue

Total revenue is the total amount of money that a firm receives from the sale of its goods. If the firm practices single pricing rather than price discrimination, then TR = total expenditure of the consumer = P × Q

Marginal revenue is the revenue generated from selling one extra unit of a good or service. It can be determined by finding the change in TR following an increase in output of one unit. MR can be both positive and negative. A revenue schedule shows the amount of revenue generated by a firm at different prices −

| Price | Quantity Demanded | Total Revenue | Marginal Revenue |

| 10 | 1 | 10 | |

| 9 | 2 | 18 | 8 |

| 8 | 3 | 24 | 6 |

| 7 | 4 | 28 | 4 |

| 6 | 5 | 30 | 2 |

| 5 | 6 | 30 | 0 |

| 4 | 7 | 28 | -2 |

| 3 | 8 | 24 | -4 |

| 2 | 9 | 18 | -6 |

| 1 | 10 | 10 | -8 |

Initially, as output increases total revenue also increases, but at a decreasing rate. It eventually reaches a maximum and then decreases with further output. Whereas when marginal revenue is 0, total revenue is the maximum. Increase in output beyond the point where MR = 0 will lead to a negative MR.

Price Ceiling and Price Flooring

Price ceilings and price flooring are basically price controls.

Price Ceilings

Price ceilings are set by the regulatory authorities when they believe certain commodities are sold too high of a price. Price ceilings become a problem when they are set below the market equilibrium price.

There is excess demand or a supply shortage, when the price ceilings are set below the market price. Producers don’t produce as much at the lower price, while consumers demand more because the goods are cheaper. Demand outstrips supply, so there is a lot of people who want to buy at this lower price but can’t.

Price Flooring

Price flooring are the prices set by the regulatory bodies for certain commodities when they believe that they are sold in an unfair market with too low prices.

Price floors are only an issue when they are set above the equilibrium price, since they have no effect if they are set below the market clearing price.

When they are set above the market price, then there is a possibility that there will be an excess supply or a surplus. If this happens, producers who can’t foresee trouble ahead will produce larger quantities.