Question: In an earlier chapter, differences between a perpetual inventory system and a periodic inventory system were discussed briefly. A perpetual system—which frequently relies on bar coding and computer scanning—maintains an ongoing record of all items present. How is the recording of an inventory purchase carried out in a perpetual system?

Answer: When a perpetual inventory system is in use, all additions and reductions are monitored in the inventory T-account. Thus, theoretically, the balance found in that general ledger account at any point in time will be identical to the merchandise physically on hand. In actual practice, recording mistakes as well as losses such as theft and breakage create some (hopefully small) discrepancies. Consequently, even with a perpetual system, the inventory records must be reconciled occasionally with the items actually present to reestablish accuracy.

In a perpetual inventory system, the maintenance of a separate subsidiary ledger showing data about the individual items on hand is essential. On February 28, 2009, Best Buy reported inventory totaling $4.753 billion. However, the company also needs specific information as to the quantity, type, and location of all televisions, cameras, computers, and the like that make up this sum. That is the significance of a perpetual system; it provides the ability to keep track of the various types of merchandise. The total cost is available in the inventory T-account but detailed data about the composition (the quantity and frequently the cost) of merchandise physically held is maintained in a subsidiary ledger where an individual file can be available for each item.

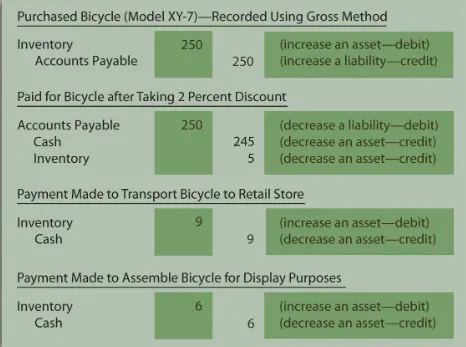

Below are the journal entries that Rider Inc. (the sporting goods company) makes for its purchase of a bicycle to sell (Model XY-7) if a perpetual inventory system is utilized. A separate subsidiary ledger file (such as shown previously) is also established to record the quantity and cost of the specific items on hand.

The assumption is made here that the transportation and assembly charges are paid in cash. Furthermore, the actual purchase is initially on credit with payment made during the ten-day discount period. The bicycle is recorded at $250 and then reduced by $5 at the time the discount is taken. This approach is known as the “gross method of reporting discounts.” As an alternative, companies can choose to anticipate taking the discount and simply make the initial entry for the $245 expected payment. This option is referred to as the “net method of reporting discounts.”

After posting these entries, the inventory T-account in the general ledger reports a net cost of $260 ($250 – $5 + $9 + $6) and the separate subsidiary ledger shown previously indicates that one Model XY-7 bicycle is on hand with a cost of $260.

Question: In a periodic system, no attempt is made to keep an ongoing record of a company’s inventory. Instead, the quantity and cost of merchandise is only determined periodically as a preliminary step in preparing financial statements.

How is the actual recording of an inventory purchase carried out in a periodic system?

Answer: If a company uses a periodic inventory system, neither the cost nor the quantity of the specific inventory items on hand is monitored. These data are not viewed by company officials as worth the cost and effort required to gather it. However, transactions still take place and a record must be maintained of the costs incurred. This information is eventually used for financial reporting but also—more immediately—for control purposes. Regardless of the recording system, companies want to avoid spending unnecessary amounts on inventory as well as tangential expenditures, such as transportation and assembly. If the accounting system indicates that a particular cost is growing too rapidly, alternatives can be investigated before the problem becomes serious. Periodic systems are designed to provide such information through the use of separate general ledger T-accounts for each cost incurred.

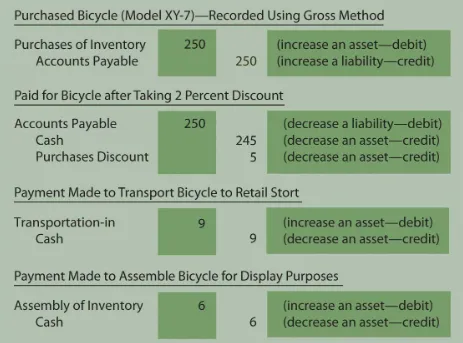

Assume that Rider uses a periodic inventory system. Its journal entries for the acquisition of the Model XY-7 bicycle are as follows. No subsidiary ledger is maintained. The overall cost of the inventory item is not readily available and the quantity (except by visual inspection) is unknown. At any point in time, company officials do have access to the amounts spent for each of the individual costs (such as transportation and assembly) for monitoring purposes.

Because these costs result from the acquisition of an asset that eventually becomes an expense when sold, they follow the same debit and credit rules as those accounts.

Note that the choice between using a perpetual and periodic system impacts the following:

I. The information available to company officials on a daily basis

II. The journal entries to be made

III. The cost necessary to operate the accounting system (the technology required by a perpetual system is more expensive